New More Secure Medicare Cards to Start Issuing in

April, 2018

The

Medicare Access and CHIP Authorization Act (“MACRA”) of 2015 requires the Centers

for Medicare & Medicaid Services (“CMS”) to remove Social Security Numbers (“SSNs”)

from all Medicare cards by April 2019. Pursuant to that mandate, the CMS announced

(Press Release dated May 30, 2017) that newly designed Medicare cards will

start issuing in April, 2018. Whereas the old or existing cards use a Social

Security number based Health Insurance Claim Number (HICN), the new cards will instead

contain a unique, randomly-assigned number called a Medicare Beneficiary Identifier

(“MBI”).

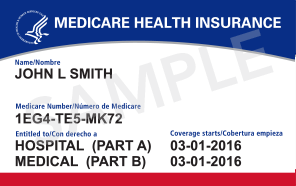

The new

Medicare Beneficiary Identifier will be 11 characters long and consist randomly

of numbers and upper case letters; the characters are “non-intelligent” which

means they do not have any hidden or special meaning. Specifically the 1st,

4th, 7th, 10th, and 11th characters

will always be numbers; the 2nd, 5th, 8th, and

9th characters will always be letters. The 3rd and 6th

characters can be either numbers or letters.

The reason for the change is to fight medical identity theft for people

with Medicare, and more generally, concern over identity theft owing to the prior

use of social security numbers. To avoid confusion, the letters S, L, O, I, B

and Z are never to be used on the new cards owing to their possible similarity

to the numbers 5,1,0,1,8, and 2. A

sample of the new card is set out below.

Issuance of the cards will be in 7 geographic waves. A list

of the planned wave strategy is set out at https://www.cms.gov/Medicare/New-Medicare-Card/NMC-Mailing-Strategy.pdf.

To be noted, here in New Jersey, a

specific date is not stated other than after June 2018.

Under

the new system, for each person enrolled in Medicare, CMS will assign a new Medicare

Beneficiary Identifier and mail out a new Medicare card to them. Thus, you will

not need to request a new card be issued. But it would be prudent to make sure

that CMS has your correct address, which may be as simple as checking the most

recent correspondence you have received from them. Note that the Medicare Beneficiary Identifier

is confidential like your Social Security Number and should be protected as

Personally Identifiable Information.

CMS

plans to have a transition period where you can use either the Social Security

number based Health Insurance Claim Number or the new Medicare Beneficiary

Identifier to exchange data with them. The transition period will begin no

earlier than April 1, 2018 and run through December 31, 2019. Starting January

1, 2020, however, you will have to submit claims using MBIs (with a few

exceptions). Your Medicare benefits are

not affected by the new cards, nor is your eligibility.

If you’re in a Medicare

Advantage Plan (like an HMO or PPO), your Medicare Advantage Plan ID card is

your main card for Medicare—you should still keep and use it whenever you need

care. However, you also may be asked to show your new Medicare card, so you

should carry this card too.

As often is the case with something new, there are persons

out there trying to scam innocent seniors. Be aware if you get calls or emails

about the new cards. Don’t give out your

personal information or financial information to strangers or those claiming to

represent the CMS, and don’t pay fees for person telling you that they will get

you the new card. As indicated above the new card will be sent to you by CMS. When in doubt, get help from someone you

trust. Also, if you have access to the internet, you can go to https://www.medicare.gov/ for information, and to http://go.medicare.gov/newcard .

From the medicare website, https://www.medicare.gov/forms-help-and-resources/your-medicare-card.html, CMS sets out the following admonition:

"Watch out for scams

Medicare will never call you uninvited and ask you to give us

personal or private information to get your new Medicare Number and

card. Scam artists may try to get personal information (like

your current Medicare Number) by contacting you about your new card. If

someone asks you for your information, for money, or threatens to cancel

your health benefits if you don’t share your personal information, hang

up and call us at 1-800-MEDICARE (1-800-633-4227). Learn more about the limited situations in which Medicare can call you."

A sample of the new card:

March 21, 2018 Barry M. Benson, Esq.